Dubai: If you were looking for more flexibility and ease when paying your loans in monthly installments, particularly when it comes to making payments in the initial months, a ‘balloon loan’ is one such choice. But how risky are they? Do they hurt your savings in the long term? Let’s find out more before choosing to use them.

A ‘balloon loan’ is a type of loan that includes lower monthly payments in exchange for a larger one-time payment at the end of your loan term. It works just like a normal auto loan except there is a larger mandatory 'balloon' payment deferred to the end of the agreement.

Let's say a person takes out a Dh200,000 mortgage with a seven-year term and a 4.5 per cent interest rate. Their monthly payment for seven years is Dh1,013. At the end of the seven-year term, they owe a Dh175,066 balloon payment.

What is one key perk or risk of taking such loans?

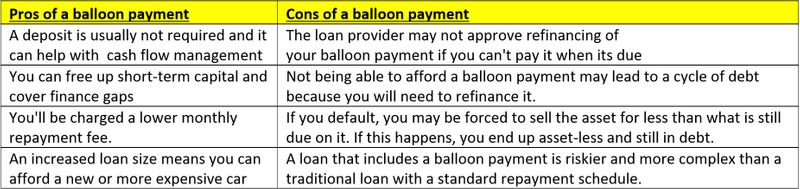

“Balloon loans often give borrowers access to a low interest rate. But the disadvantages often outweigh the positives, as there is no guarantee that the borrower will be able to refinance at that same lower rate – or will be able to refinance the loan at all,” said Bryden Wood, a Dubai-based banking analyst.

“There are also drawbacks to balloon payments that should be considered: Unsecured loans with balloon payments usually have a higher interest rate than conventional loans. Paying that large balloon payment at the end of the loan may be financially difficult for your business,” Wood further explained.

Is there a downside in taking a balloon mortgage?

When it comes to a balloon mortgage, the term is usually rather short, ranging from 5 to 7 years, but the payment is based on a term of 30 years. They often have a lower interest rate, and it can be easier to qualify for than a traditional 30-year-fixed mortgage. There is, however, a risk to consider.

“If the value of your property declines, you lose your job or face another financial hardship, you may not be able to sell or refinance before the balloon payment comes due. If you can't make the payment, you risk losing your home to foreclosure,” added Wood.

Is there a cap on balloon payments allowed?

“Although balloon payments are all about paying off a significant chunk of your loan at the end, they're usually capped,” explained Parthiv Patnaik, a Dubai-based banker with nearly four decades of experience.

“Generally speaking, most lenders will cap balloon payments at 50 per cent of the total amount payable. So, if you're looking to buy a Dh30,000 car, your balloon payment couldn't be higher than Dh15,000.”

Are there any other alternative to balloon loans?

There is another similar option which requires less of a commitment from you than a balloon payment – a residual value loan. But what is the difference between residual value and balloon payment?

Put simply, a residual value and a balloon payment are the same. Both refer to a pre-agreed payment due at the end of a loan for a vehicle, machine or property. If the loan facility was a finance lease, then the amount at the end of the lease is called a residual.

You'll still pay a monthly amount during your lease period, just like you would for a balloon payment; but you're not committing to buying the car at the end. If you choose to, you can return the car to the vehicle finance provider or sign a new lease deal for it and continue to lease it for another set period.

Residual loans better for new or second-hand cars?

“When using residual value loans, buyers can get lower premiums on new cars, but second-hand cars could have higher monthly premiums because their value usually depreciates more,” added Patnaik.

“The loan provider may monitor the number of kilometres you travel in the new car and could penalise you for high mileage or a lack of maintenance. This is because a car's mileage and condition affect its resale value.”

Bottom line: Is a balloon payment a good idea?

For buyers who can save the amount needed, a balloon payment can work to their advantage, and for investors, it can free up short-term capital. In most cases, however, balloon repayments are an easy way to find yourself in debt.

Most people who are average income earners that can't afford the original repayment amount can also not accrue the amount needed to pay the lump sum at the end of their repayment period.

“It isn't always easy to think about the long-term ramifications of balloon payments. Many people know how easy it is to go over their budgets when they have their hearts set on a specific car or property, especially when a balloon payment option looks so attractive,” added Wood.

“Unfortunately, people in this position often can't pay the lump sum at the end of the finance term and debt problems follow. As a safeguard against this, financing companies often require evidence that buyers will be able to afford a future balloon payment.”