Shelter for your assets

Despite tightening tax avoidance rules worldwide, there remain many countries where you can stash your cash

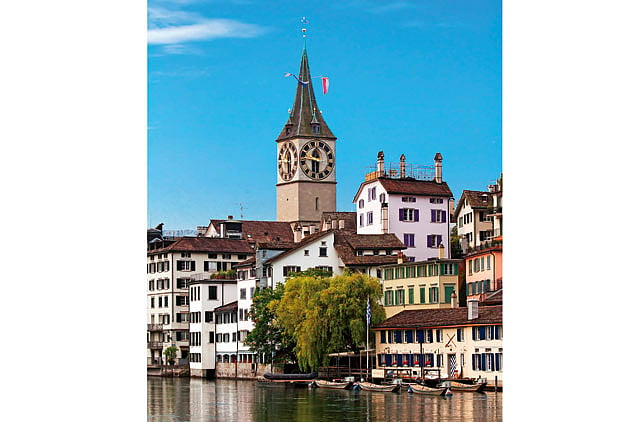

Switzerland is without a doubt the world's best tax haven. With its reputation for discreet bankers and maintaining the highest levels of secrecy, the alpine country has over the decades become a safe location to deposit money, which otherwise would have drawn the attention of tax authorities in the country of origin.

However, with the European debt crisis putting many governments in financial distress, the era of safe tax-free deposits seems to be gone, at least partly. The European Union has recently drafted new bilateral tax agreements for Switzerland and other European tax havens such as Liechtenstein, Andorra, the Channel Islands and the Isle of Man.

Ever since the German Finance Ministry got hold of a compact disc with details of thousands of German citizens who have clandestinely transferred untaxed money to Swiss banks, all hell has broken loose in high-net-worth circles.

Fighting tax avoidance

European Union Tax Commissioner Algirdas Semeta said last month in a speech to the EU Commission that the bloc needs "to go further" in fighting tax havens and "aggressive" tax planning so that businesses and companies pay what they owe.

Tax avoidance is an issue not only in Europe but also in emerging countries with growing wealth among its citizens. India, for example, is debating on whether to include new general anti-avoidance rules as part of the Finance Bill 2012 to combat growing tax evasion and aims to review all double taxation avoidance agreements the country has signed including the one with the UAE.

On April 16, India and the UAE signed an agreement in Abu Dhabi to amend the double taxation avoidance treaty, paving the way for greater sharing of tax-related information. After ratification, banking information as well as any information regarding tax interest will be shared between the two countries.

Foreign investors have also been concerned about the proposed anti-avoidance rule as it could override India's tax treaty with the tax haven of Mauritius, which exempts capital gains from being doubly taxed. Most foreign funds invest in Indian stocks and bonds through Mauritius.

"The purpose of the new regulation is not to target a particular country or foreign institutional investor, but all those who are assessed are liable to pay tax in India, whether it be foreign parties or Indian companies," India's Revenue Secretary R.S. Gujral said after public outcry over the new draft rule.

However, it might be a prejudice to judge a tax haven by its facilities to avoid paying owed tax in the first place. A tax haven primarily is a state or a country where certain, mostly individual, taxes are levied at a low rate or not at all, which makes such a territory interesting for people who want to transfer funds that have already been legally taxed in the country of origin just because of the more favourable parameters offered.

There is nothing wrong if somebody transfers his life savings to a tax haven to withhold tax on interest earned, personal income tax on funds withdrawn, and legally avoid other personal taxes such as capital gains tax, inheritance tax or estate duty, capital transfer tax, gifts tax and wealth tax.

Individuals may do so to either have peace of mind for their future financial planning, settle down in a tax haven, or having turned into perpetual travellers after retiring early, need a base for their funds outside their home country.

In Europe, some countries have still preserved such conditions for individuals. While Switzerland isn't exactly a tax-free country but rather a tax haven, options exist in some countries such as Andorra and Monaco that offer a zero per cent personal tax policy, or Liechtenstein and Cyprus with their lower-than-average European tax rates.

The Channel Islands, Jersey and Guernsey, as well as the Isle of Man have a favourable zero tax regime for companies, but charge between 10 and 20 per cent personal tax on income.

Worldwide, identifying a tax haven depends on the definition. No two commentators can generally agree on a list of tax havens, but the classic perception of a sovereign tax haven includes zero per cent corporate and personal income tax and related taxation, as well as the absence of foreign currency controls.

Small, affluent centres

While the US National Bureau of Economic Research suggests that roughly 15 per cent of the world's countries can be classified as a tax haven, a zero tax regime is harder to find. Most of these countries, which can be found in Central America and the Caribbean and increasingly, in Asia, tend to be small and affluent and do not need to charge as much as some industrialised countries to earn sufficient income for their annual budgets.

Panama, for example, was for North America what Switzerland was for Europe — a discreet tax and money haven. With a relatively stable government, a fixed dollar rate to its own currency, and good infrastructure, at least around the capital where all the banks and the new property developments were, it attracted billions of funds.

However, since some banking scandals — which mainly involved Columbian drug money deposited in the country, many Panama banks are as a general rule no longer opening accounts for people from the US, Russia and African nations (except South Africa) among others.

Some banks in Panama now also request customers to sign waivers of bank secrecy and report financial information to taxation authorities abroad.

Other countries in the region such as the Cayman Islands and British Virgin Islands have certainly retained a higher level of secrecy, as well as Belize, Bermuda and the Bahamas, which are all more or less tax-free for foreign depositors and generally safe.

Smaller nations such as St Kitts and Nevis, Turks and Caicos, and St Vincent and the Grenadines offer similar financial freedom, but might not be the first choice for someone unfamiliar with the Caribbean hemisphere.

In the US the states of Delaware, Nevada and Wyoming have a company-friendly tax regime, but US individuals might prefer the US Virgin Islands to transfer their funds.

Asian hubs

At the other end of the world, Asia boasts traditional tax havens with a long-lasting reputation for safety and stability such as Singapore and Hong Kong, followed by the Malaysian island of Labuan that defines itself as an offshore finance hub for South East Asia.

Nearby, the small Sultanate of Brunei has recently taken measures to become a new financial offshore hub for companies and the distressed high-net-worth community by establishing an International Offshore Financial Centre, where international business companies can be registered and discreet bank accounts can be opened.

Elsewhere in Asia, the Seychelles, the Maldives and the Philippines rank high in the financial secrecy index and their easy-going tax regime for foreigners.

In the Middle East, the main offshore finance centres can be found in the UAE, mainly in Dubai and Ras Al Khaimah, with their generous tax-free environment for individuals and most companies as well as in the world's largest free trade zone, Jebel Ali Free Zone. Bahrain and, to a certain extent, Lebanon are also attractive options.

While the UAE does not need much explanation as to why it is a tax-free paradise, Bahrain, with a similar zero tax regime for individuals, is also focusing on luring offshore companies into the country. However, the current unrest in the country has put a serious damper on these ambitions.

Prior to the rise of some Gulf states as tax havens, Lebanon had a reputation for being the offshore finance centre of the Middle East. However, political and economic deterioration as well as security issues eroded this status despite the country still hosting favourable conditions for individuals and companies.

Sign up for the Daily Briefing

Get the latest news and updates straight to your inbox

Network Links

GN StoreDownload our app

© Al Nisr Publishing LLC 2026. All rights reserved.