Elliott increases pressure on BHP to ditch petroleum

BHP petroleum business has value of more than $20b

Sydney, London: Activist investor Elliott Management raised the pressure for strategic changes at BHP on Tuesday, calling for an independent review of the mining giant’s petroleum business.

Elliott, which has built up a 4.1 per cent stake in BHP’s London-listed arm and is urging changes to boost shareholder value, said there were clear signs the market was receptive to a new strategy for BHP.

“There is extremely broad and deep-rooted support for proactive steps to be taken by management to achieve an optimal value outcome for BHP’s petroleum business following a formal open review,” it said in letter to management.

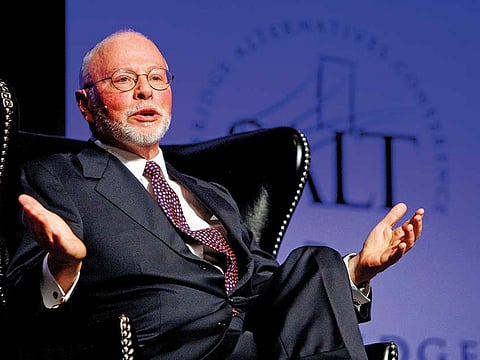

Elliott, founded by billionaire Paul Singer, has been pushing for BHP to collapse its dual-listed structure, spin off its US oil and gas assets, and boost returns to shareholders since publishing its proposals on April 10 — all of which BHP has rejected.

Its latest letter, which did not name any other shareholders, was released hours before BHP chief executive Andrew Mackenzie spoke at a Bank of America Merrill Lynch mining conference in Barcelona that is also being attended by Elliott.

BHP said it was disappointed Elliott believed the company was not open to suggestions and dismissed criticism that it had been misleading in its response to the New York-based investor’s calls for a change in strategy.

“We reject both claims,” the miner said in an emailed statement, adding that it would review Elliott’s latest material in full and formally respond.

Speaking at the Barcelona conference, which is attended by bankers and investors, Mackenzie said BHP had made consistent progress and was confident it could grow the value of the company by up to 50 per cent and almost double the return on capital.

“Our path is deliberate, with value and returns at the centre of everything we do,” Mackenzie said in a copy of his speech.

He said BHP’s petroleum exploration programme had a value of more than $20 billion (Dh73.64 billion) and close to a quarter of this was in low-to-medium risk prospects to be tested in the next two years.

Mackenzie has previously said it is the wrong time for BHP to sell its US petroleum assets, given oil prices are still relatively low at about $52 per barrel.

BHP has also sought to highlight the action it is taking to divest non-core parts of its US shale assets.

Meeting in Barcelona

A source close to BHP said the company expected to meet Elliott in Barcelona.

Analysts at Deutsche Bank and Citi have said BHP could unleash billions of dollars by selling part or all of its petroleum business, although Citi cautioned this would bring only a one-off benefit to shareholders and the company should focus on how to grow value for investors.

“The current period of shareholder activism could result in a break-up and/or a significant alteration of the company’s structure,” Citi said in a note this week.

Responding to concerns raised by the Australian government, Elliott on Tuesday backtracked on its proposal for BHP to have its main listing in London, saying that it could remain incorporated in Australia and stay an Australian tax resident, retaining full listings on the Australian and London bourses.

An example would be International Consolidated Airline Group, which resulted from the 2010 merger of British Airways and Iberia. IAG has its primary listing in Spain but also trades in London and remains part of the benchmark FTSE 100 index.

BHP has said the costs of scrapping its dual-listed structure significantly outweigh the benefits.

Its share price has fallen since Elliott launched its attack in April and the London stock is down nearly 9 per cent since the start of the year. By 0730 GMT on Tuesday, BHP was down 0.2 per cent.

On its website, fixingbhp.com, Elliott also criticised BHP’s track record on share buy-backs and suggested the company make a $6 billion buy-back in 2018.

Such a buy-back, if the current valuation remained unchanged, would lead to $2.4 billion in value accretion, equivalent to more than 12 times Elliott’s expected costs of unifying BHP’s dual listings, it said.

Elliott has put the cost of unification at $200 million and said BHP’s $1.3 billion estimated cost was “flawed and misleading”.