UAE residents lament falling into debt traps

Debtors recount ordeal of easy loans that proved tough to repay

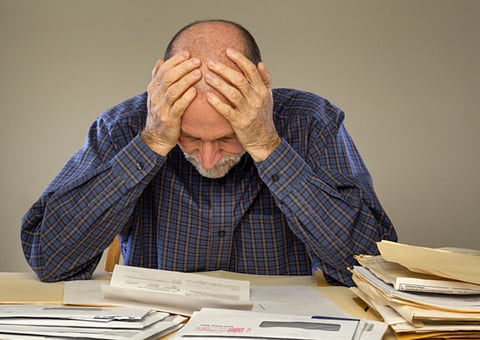

Dubai: Residents overburdened with debt have spoken of their ordeal, with many blaming banks for coming down hard on customers who were “pushed” to take out huge loans in the first place.

They complained banks are laying debt traps, by granting relatively large loans and credit cards to customers with limited income, who then struggle to return the piling interest and late payment fees – with disastrous results in many cases.

Many residents continue to be jailed for bouncing post-dated or “guarantee” cheques – a crime here as opposed to a civil case in the wider world – which they had to write out as repayment terms. And with no bankruptcy protection under current laws, expat debtors often make the choice to flee rather than go behind bars.

Unable to cope, some residents have committed suicide, while others have gone underground.

The problem, debtors told Gulf News, is that credit has been made too easy to obtain but too hard to clear once repayment schedules breakdown in unforeseen circumstances. Many of those who contacted Gulf News about their cases said they were ordinary employees who were offered loans and credit cards worth hundreds of thousands of dirhams.

They claimed there were “pushed hard” to accept the debt products, an offer that was not difficult to accept as they happened to be in a financial crunch. Job loss, health emergency, death of a family member, rising rent, school fees – the list of reasons cited by them were varied and long.

Some defaulters also spoke of landing in a catch 22 situation – being unable to repay because of being laid off and being unable to land work because of being a defaulter in a criminal court case.

Job loss

A Pakistani father of one said he has been to jail twice – and maybe facing a third sentence – after being unable to repay loans following his job loss. He added that his loans had piled up to about Dh1.4m from six credit cards, a mortgage, and a personal loan when he was working as a mid-level executive in a leading property company in Dubai.

“When times were good, banks were calling me to keep signing up for more and more credit. Now, they keep calling for the repayment money. They know I don’t have a proper job, I haven’t fled the country. I’m doing freelance work in web development; give me some slack so I can pay you back. I can’t do that from jail, can I?” he said.

“I’ve sent my family back home as they can’t cope with the idea of me going back to jail. I spent about two months inside for two bounced cheque cases. My mortgage lender had filed a case the second day they found out I had been downsized – how will that help them recover the money from me?”

An executive from a leading bank said the rules say a customer cannot be granted loans more than 50 per cent of their income. But different banks offer multiple loans to the same client, and products like credit card limits are increased for those with good repayment records.

The banker added that banks can check with the UAE Central Bank the total debt obligations of customers regardless of how many other banks are involved. But debtors told Gulf News of being offered Dh300,000 loans and credit cards despite drawing modest monthly salaries of Dh10,000-Dh15,000.

A young Indian who makes about Dh13,000 a month is spending virtually the entire salary in paying back debts, and surviving on friends’ help.

He said he owes about Dh500,000 to four banks in personal loans and six credit cards. “I had a lot of family problems: my mother died, my relatives needed money. My banks kept extending the credit lines, but I never thought things would get so bad,” he added.

The bachelors said about 15 post-dated cheques written by him have already bounced.

“I’m under constant threats of jail made by debt collection agents. I’m distressed, I can’t work properly. I still have 130 cheques that will need to be cleared. And then there are four guarantee cheques with no dates for four separate loans they can use anytime against me.”

He added: “You can’t tell people, ‘don’t go to the bank in emergencies.’ Where else will they go? But the banks should either not give you so much money if you’re just a simple man like me, or they should understand that circumstances change and it’s not possible for everyone to pay on time every time.”

One such bank customer who faced a series of ‘emergencies’ is a 40-year-old Filipino man who racked up 16 credit card limits and has four legal notices against him.

“I’m not a bad person. I ended up taking up all these loans because of several misfortunes in our family that I being the eldest carried the responsibility to fix,” he said in a letter to his employer. The debtor has since gone into hiding.

He said problems began in 2006 when his sister’s husband was shot in the Philippines and he took over their family expenses, going deeper in debt with Dubai banks to accomplish that.

In 2007, his wife gave birth to a second son and his mother lost her job in Athens. A year later, his nephew was diagnosed as being autistic and need to be placed in a school for children with special needs. And in 2011, his son too was found to be autistic and needed special – more expensive – schooling.

“As bad as it may seem, taking those loans were my only options to help me save my family’s needs.” He added that he has to pay back about Dh500,000 or face jail.

Another Filipino, an office assistant, is on the run from creditors and police. He stays with friends, moving places, and is irregular at work, where police officials had recently showed up to question him.

Visa expired

He is wanted for bouncing a Dh20,000 cheque and still has outstanding debts worth about Dh200,000. He failed to get a loan buy-out because he was only about Dh25 short of a minimum salary requirement of Dh8,000. The debtor added that neither his employer nor his bank have yet helped him to meet or waive this amount so he could clear his earlier cases.

“My passport is with the police. My visa has expired, I can’t get a new job with a higher salary. The bank has a case against me – so how I pay them back in such a situation?” he said.

“My father died in 2010 back home and I’m still unable to even pay my respects at his grave. I’m stuck in a limbo, I’m scared I’ll go to jail anytime."