Dubai: Saudi Arabian banks are expected to post "mild earnings performance" for the third quarter of this year as they focus on minimising risk, analysts said.

Recent statistics showed that additional profit in August was 2.7 billion riyals, a 4.4 per cent decrease from the previous month, bringing July and August combined profits to 5.4 billion riyals.

This is 78 per cent of aggregate earnings posted by Saudi banks in the second quarter, data collated by analysts at Dubai-based Shuaa Capital show.

"Banks are continuing to shy away from lending to focus on optimising funding allocation and ultimately lower their balance sheet risk profile. Instead of using their comfortable liquidity to instigate new lending, Saudi banks are electing to tighten their liquidity position by forgoing deposits," Shuaa analyst Sofia Al Boury wrote in a note to investors.

"This move is most probably designed to preserve margins as shedding expensive deposits allows banks to bring down funding costs. As such, ‘plain vanilla' loans-to-deposits ratio has increased from 81 per cent in July to 83 per cent at August-end."

From December 2009 to August 2010, deposits at Saudi banks slipped by two per cent, in complete contrast to Shuaa's forecast of a 10 per cent increase.

Desirable improvements

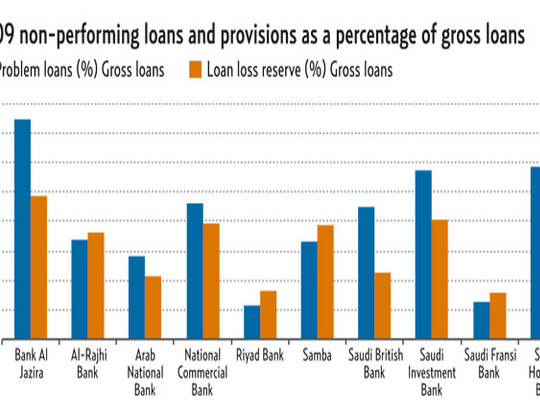

"The banks' risk management has been improving and their corporate governance culture has been strengthened, while their already moderate risk appetite has further diminished," said Christos Theofilou, analyst at rating agency Moody's Investors Service.

"These factors have helped improve the banks' risk profiles, although ongoing improvements are desirable. In particular, Saudi banks have high concentrations on both the asset and liability sides of their balance sheets," he said.

While the banks remain sufficiently liquid and funded by "sticky" local deposits and their profile reduces market funding-related vulnerabilities, challenges include high concentrations in deposits and mismatches in the maturity profiles of assets and liabilities, Theofilou wrote in a note to investors.

August interbank liabilities in Saudi Arabia lost 12 per cent, or 3 billion riyals, over July, to end the month at 22.5 billion riyals. Foreign liabilities increased 11 per cent over July to 94 billion riyals, according to Shuaa data.

The deposit slump comes after a relatively strong pick-up in May and June and preservation of this growth in July. The total deposit base of Saudi banks at the end of August stood at 925.9 billion riyals.

Apart from shying away from increasing deposits, banks remain wary of lending. During August, private sector claims reported a negligible increase of 0.3 per cent over July to a total of 766.8 billion riyals.

"Overlooking abundant liquidity and demand for credit, banks seem persistent in maintaining strict control over lending standards and terms. Alternatively, they remain supporters of liquid assets," said Al Boury.

Theofilou added: "Catalysts for potentially greater lending activity could include the banks' strong liquidity and expectations of a peak in provisioning levels, in conjunction with banks' efforts to maintain market share and margins in the current low-interest/low-growth environment.

"Indications already point to a pick-up in loans to the private sector, with a healthy pipeline of projects expected over the next 18 months, which — coupled with the banks' growing emphasis on retail banking — is conducive to stronger private sector growth.

Strengths

- Most Saudi banks have solid local franchises that benefit from their extended operations and product base, and increased focus on retail and Islamic banking.

- Sound capitalisation and conservative reserve coverage levels, in conjunction with adequate profitability, enable banks to absorb losses.

- Saudi banks have strong liquidity ratios and are funded by "sticky" local deposits, which reduces vulnerabilities related to market funding.

- The government's robust financial position and commitment to an expansionary budget have lent support.

- A prudent and strict regulator.

Challenges

- Corporate activity is dominated by a small number of very large groups, which are themselves relatively dependent on government activity, leading to high credit concentrations.

- Mismatches in the maturity profiles of assets and liabilities and high funding concentrations could create funding and liquidity management issues.

- Geopolitical instability and security threats remain potential areas of concern, as do the economy's still limited diversification.

— Source: Moody's Investors Service