Dubai: Do you know where your salary goes after each month or do you scratch your head and wonder where it disappears to?

If you’ve been working overseas for several years now, do you have anything of value to show for it? Apart from the extra pounds and grey hair you’ve accumulated, of course.

But the last part — the savings part — does not come easy for all, it seems.

In a poll, Gulf News asked 2,548 people if they would be able to produce Dh1,000 right away for an emergency if it’s not pay day and they’re not allowed to borrow from anywhere. Simply put, if they have at least Dh1,000 tucked away for an emergency.

Some 50.11 per cent said they don’t have even Dh1,000 saved up while the remaining 49.88 per cent said they do.

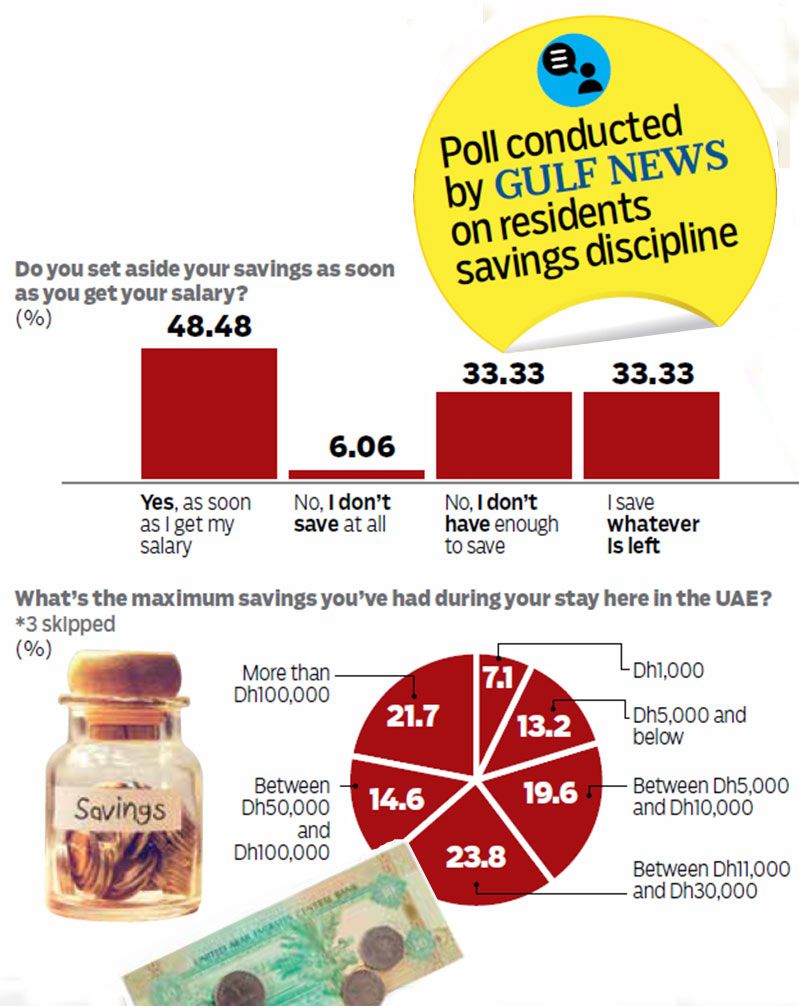

In another Gulf News survey of 100 residents, nearly half of the respondents said savings is a priority that is why they automatically set aside their savings after getting their salaries while the 33.33 per cent said they save whatever is left.

The bad news is nearly two out of 10 or 18 per cent said they don’t have enough money after each month to save or they don’t save at all.

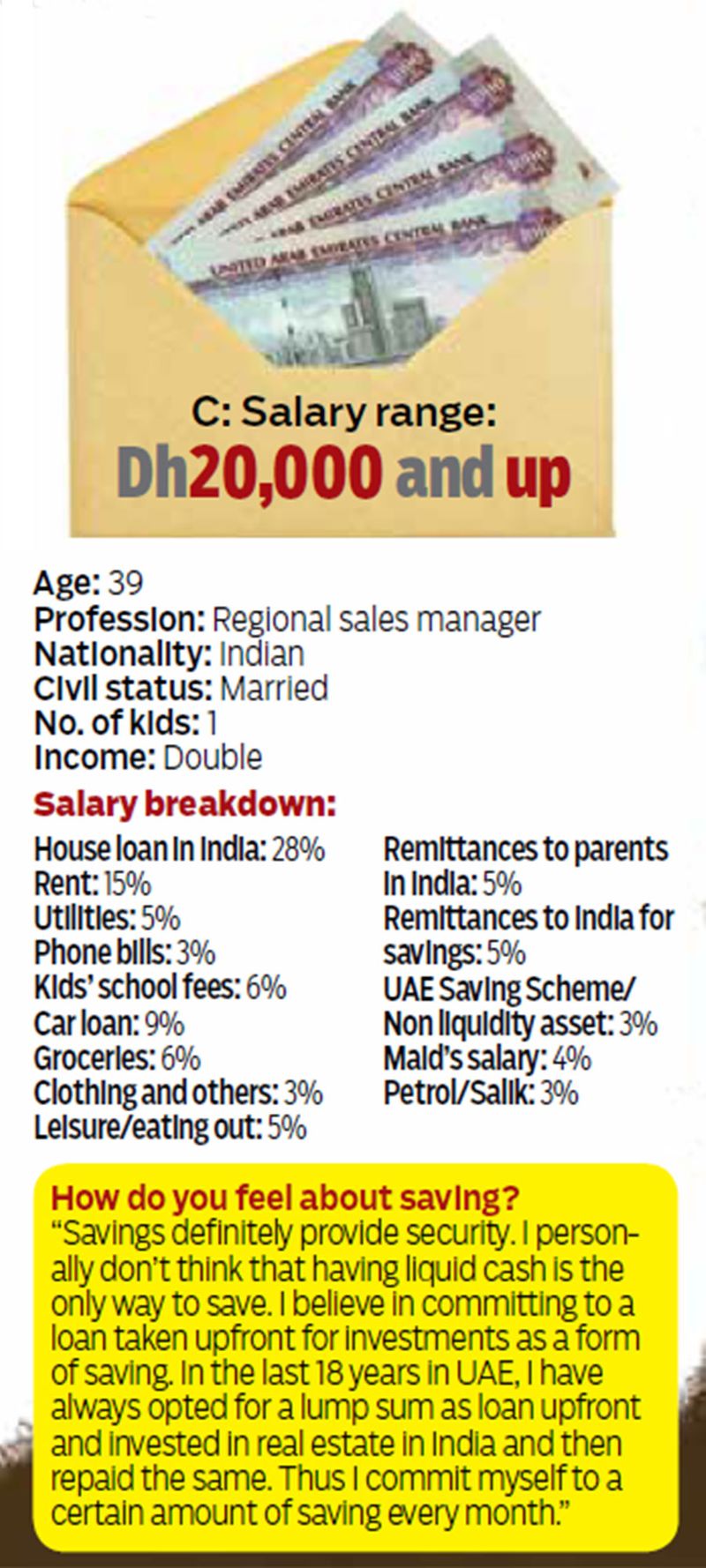

Survey

In 2016, a survey on the saving habits of 2,200 UAE residents by compareit4me, a finance comparison site, revealed that 53 per cent of respondents believe they do not earn enough money to be able to save anything.

Rupert Connor, a financial planning adviser at Abacus Financial Consultants, said: “Savings is a priority for my clients because they’re serious about protecting their family and saving for the future. For a lot of people, it’s not a priority.”

“By and large, most people know they have to save. It might not be at the top of their priority list but they know deep down they need to do it,” he added.

The question is whether they’re actually doing it.

When writing this special report, discussing savings and finances was a particularly sensitive topic for most expatriates, Gulf News found.

People didn’t want to discuss their finances openly due to many reasons.

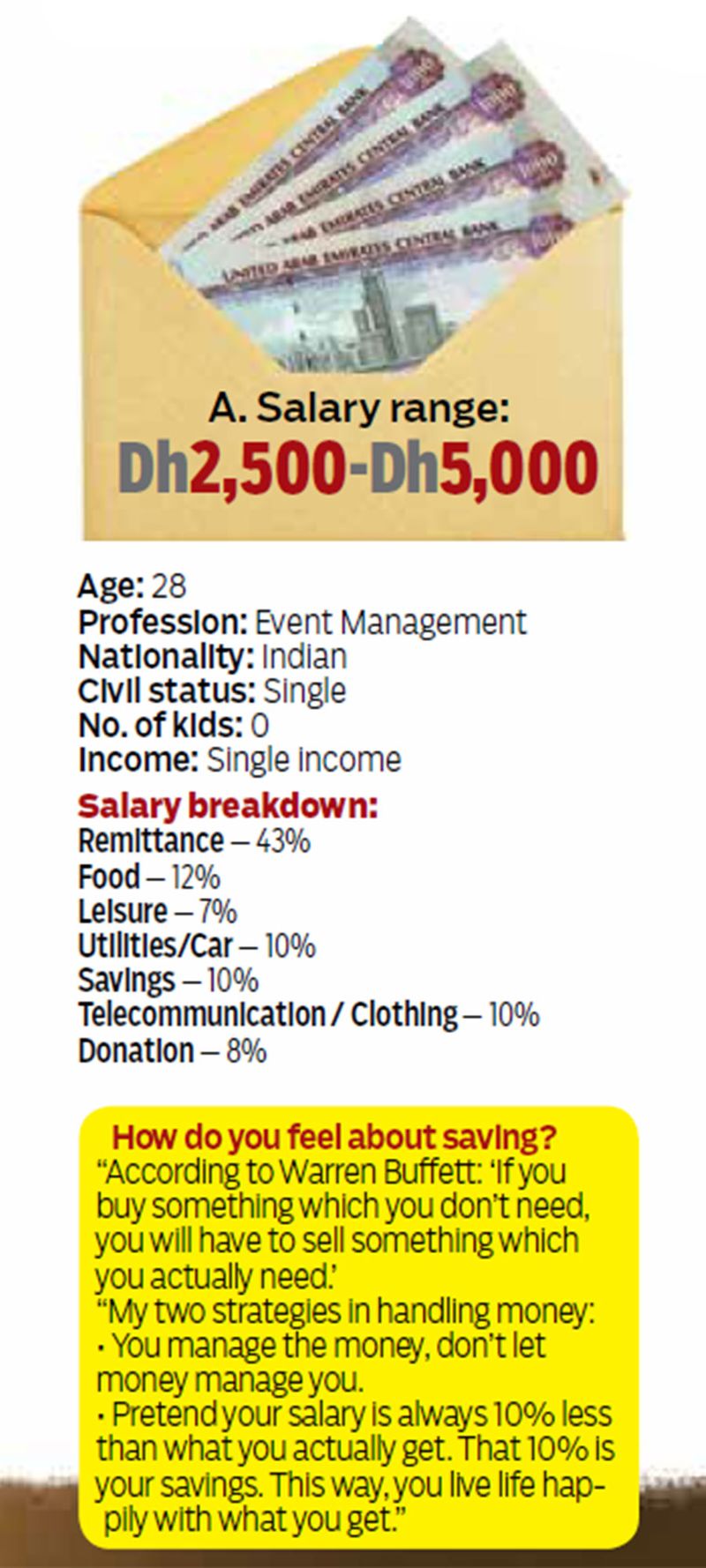

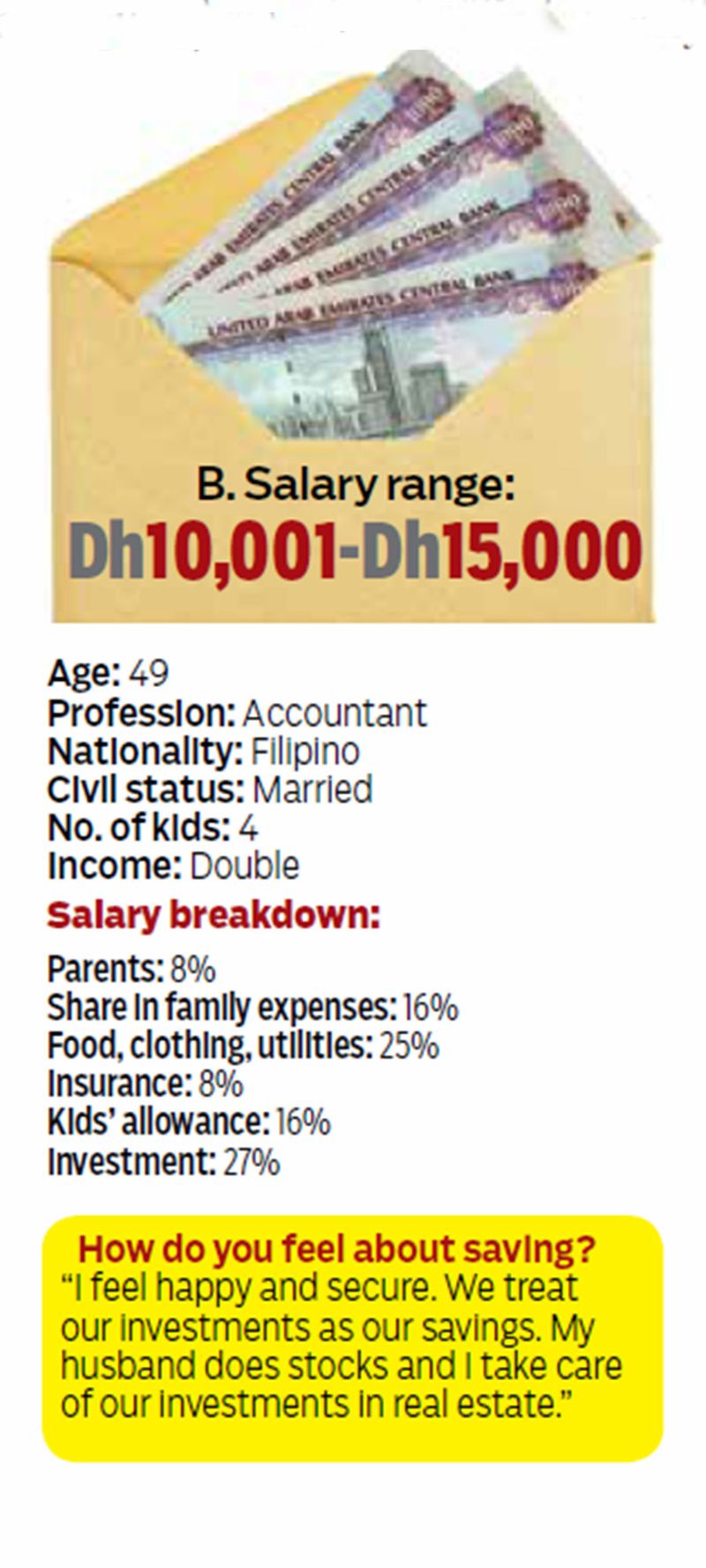

Based on the poll, some 31 per cent of the respondents said more than 50 per cent of their income goes to living expenses such as shelter, food, clothing, utilities, and transportation.

Expenses pie

The biggest chunk of their income goes to the following, in order of importance and as a share of income:

rent or mortgage followed by food and groceries.

- Rent or mortgage

- Food and groceries

- Loan and credit card repayments

- Children’s education

- Utilities

- Remittances

- Savings

- Investments

But it’s not the amount that you set aside but the discipline to treat savings as an expense or as part of the budget that’s important.

Saving for emergencies and future purchases is one thing, saving for retirement is another. But both require intentionality.

In 2015, a survey by Zurich International Life found that only 33 per cent of UAE residents have a formal retirement plan.

This has somehow changed — but just a bit, Susan Francisco, a financial adviser at Nexus Insurance Brokers, said.

Compared to two years ago, most residents now are more open to the idea of saving and investing for the future based on the financial literacy seminars she conducts and attends.

The major issue preventing some people from saving now is loan repayments and the high cost of living, she said. But this is not an excuse.

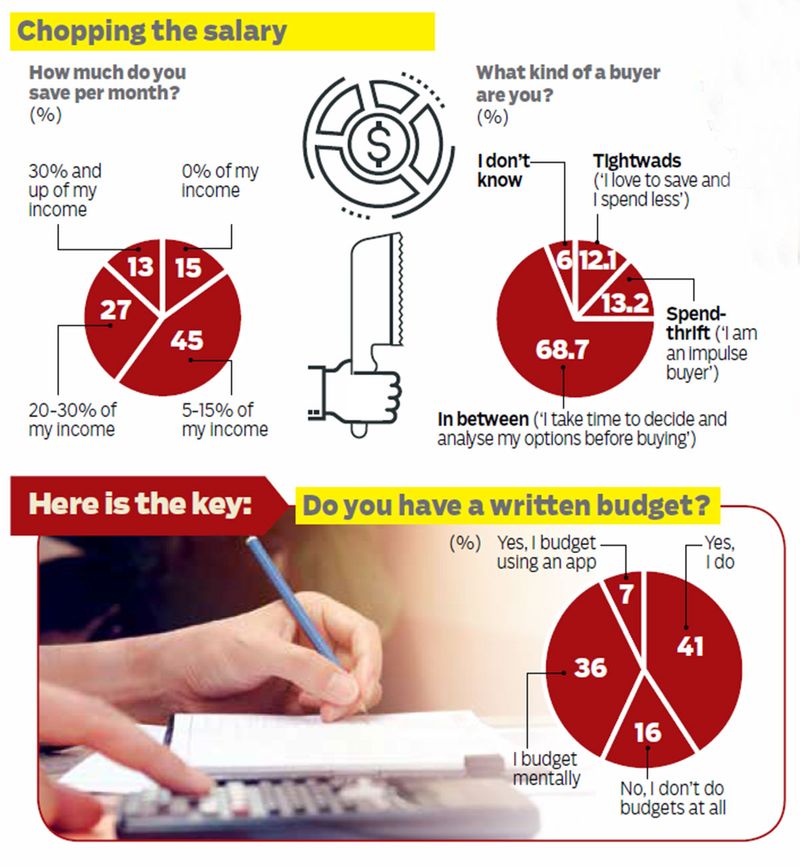

Most financial advisers say 10 to 30 per cent of your income saved up is a good amount.

For Francisco, the better allotment per month is 60 per cent for expenses, 20 per cent for savings and 20 per cent as Emergency Funds. And the last two should never mix.

“You have to muster every ounce of self-discipline you can get to limit your outgoings and increase your savings and cash flow. Imagine, if you’re young and healthy now, you won’t stay that way forever. What about 10 to 20 years from now? If you fall ill and suddenly become unable to work, how will you and your family survive?”

“Plan, save, invest, and protect your savings, that way you’re protecting your family, too. Always think beyond the here and now.”

Poll conducted by Gulf News on residents' savings discipline

Monthly expenses

In our poll, we asked: "What do you spend your monthly salary on? Rank them from biggest to lowest."

The poll revealed the following priorities:

- Rent/mortgage

- Food/groceries

- Loan/credit card payment

- Children’s education

- Utilities

- Remittances

- Savings

- Investments

- Shopping/entertainment

- Eating out